By LaimRefund Team · June 02, 2026

Krispy Kreme Data Breach Settlement 2026: How to Claim Before June 22

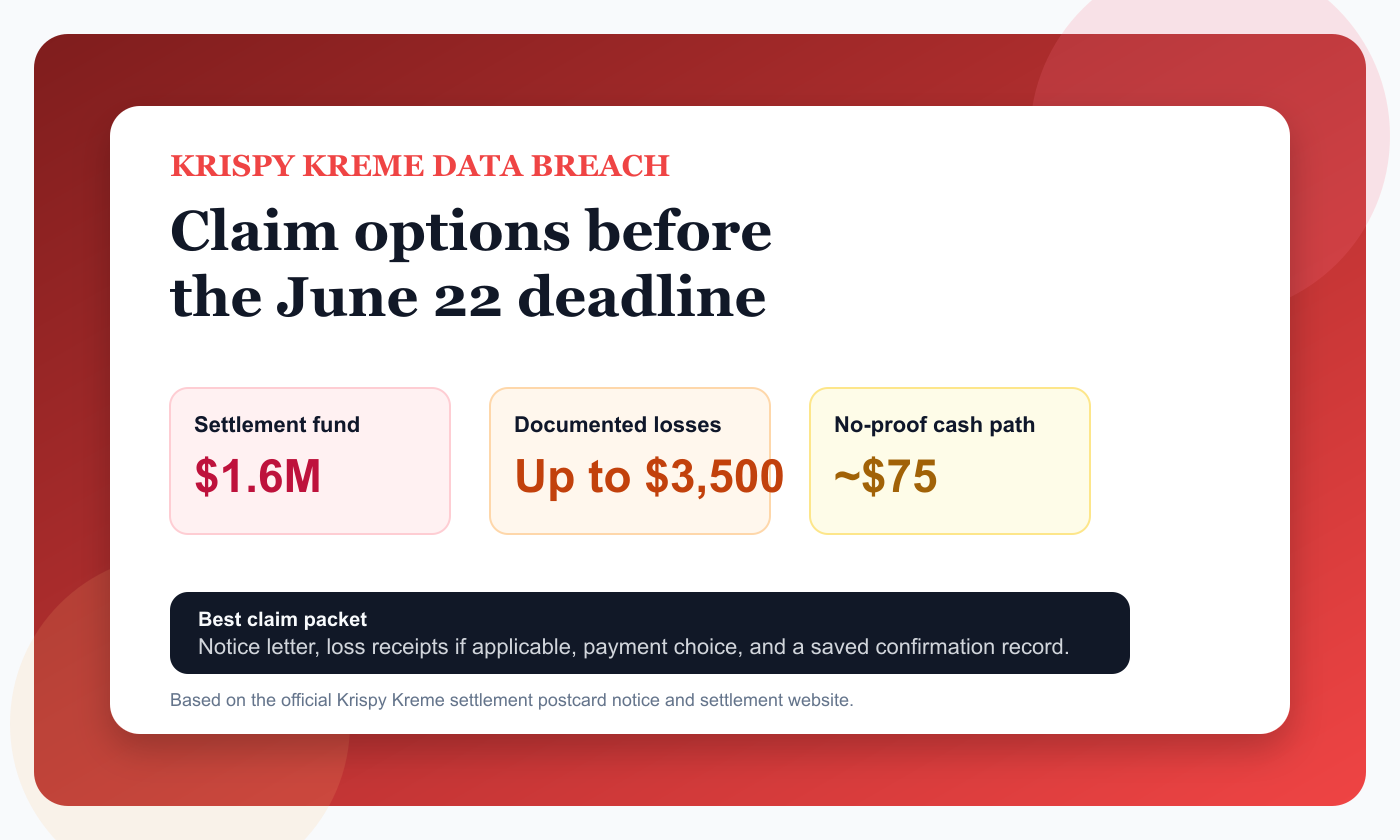

The Krispy Kreme data breach settlement gives consumers a classic fork in the road: file for documented losses up to $3,500, take the alternate cash payment, or at minimum activate the free credit monitoring. The right choice depends on your proof, your timeline, and whether you actually incurred fraud or identity-theft-related costs.

Introduction and Main Problem Explanation

The official Krispy Kreme settlement postcard notice says a $1,616,760 settlement was reached regarding a Data Incident discovered on November 29, 2024, and that claim forms must be submitted online or postmarked by June 22, 2026. The notice says class members who were sent notice may choose Cash Payment A for documented losses up to $3,500, or Cash Payment B for an alternate cash payment estimated at about $75 without documentation. It also says one year of free credit monitoring is available.

This kind of settlement is where many consumers accidentally leave money on the table. They hear the maximum number, rush toward the biggest figure, and then realize they do not have proof that connects their losses to the breach. Other people do the opposite: they take the smaller no-proof cash option quickly even though they have bank fees, fraudulent charges, tax-filing costs, or credit repair expenses that could support a larger documented-loss claim.

The decision is not only about money. It is about claim friction. A documented-loss claim takes more work because the administrator will want reasonable documentation. That usually means statements, invoices, fraud reports, receipts, or records showing time and expense tied to identity theft or fraud more likely than not caused by the incident. The alternate cash claim is easier, but it is intentionally smaller.

The settlement also includes monitoring, which many people ignore because they focus only on the payout. That can be a mistake. If your information included sensitive identifiers, monitoring can be the most practically valuable benefit, especially if you have not seen fraud yet but still need an early-warning layer.

The fastest way to lose money in a settlement is to confuse the claim path with the story path. The story path is what happened to you. The claim path is what the administrator actually needs to approve payment: a class definition match, a deadline, and the right identifiers.

Consumers also tend to over-assume that a no-proof claim means no records matter. In reality, records still protect you if the administrator asks follow-up questions, if your notice was lost, if your address changed, or if you later need to choose between a flat payment and a documented-loss claim.

A disciplined file usually includes five things: the notice email or letter, the official settlement URL typed directly into the browser, a screenshot of the important dates page, any receipts or statements tied to the issue, and a copy of the final claim confirmation. That packet is much more useful than relying on memory weeks later.

Scam risk is part of the workflow now. Real settlements often look odd because they use standalone domains, third-party administrators, and claim IDs. That means a legitimate notice can feel suspicious. The safe move is not to ignore every message. The safe move is to verify the case name, administrator, deadline, and official website before you type anything.

Search demand around these topics is practical and urgent. People search for whether a settlement is real, what deadline applies, whether proof is required, how much documented losses are worth, and whether they can still sue if they do nothing. A strong SEO article has to answer those concrete questions in plain language.

This topic works well for SEO because it serves two kinds of searchers at once: people who want to know whether the notice is real, and people who are already halfway through the form and want to know which payment option makes sense. Those are high-intent readers, and they need specificity more than hype.

Step-by-Step Guide

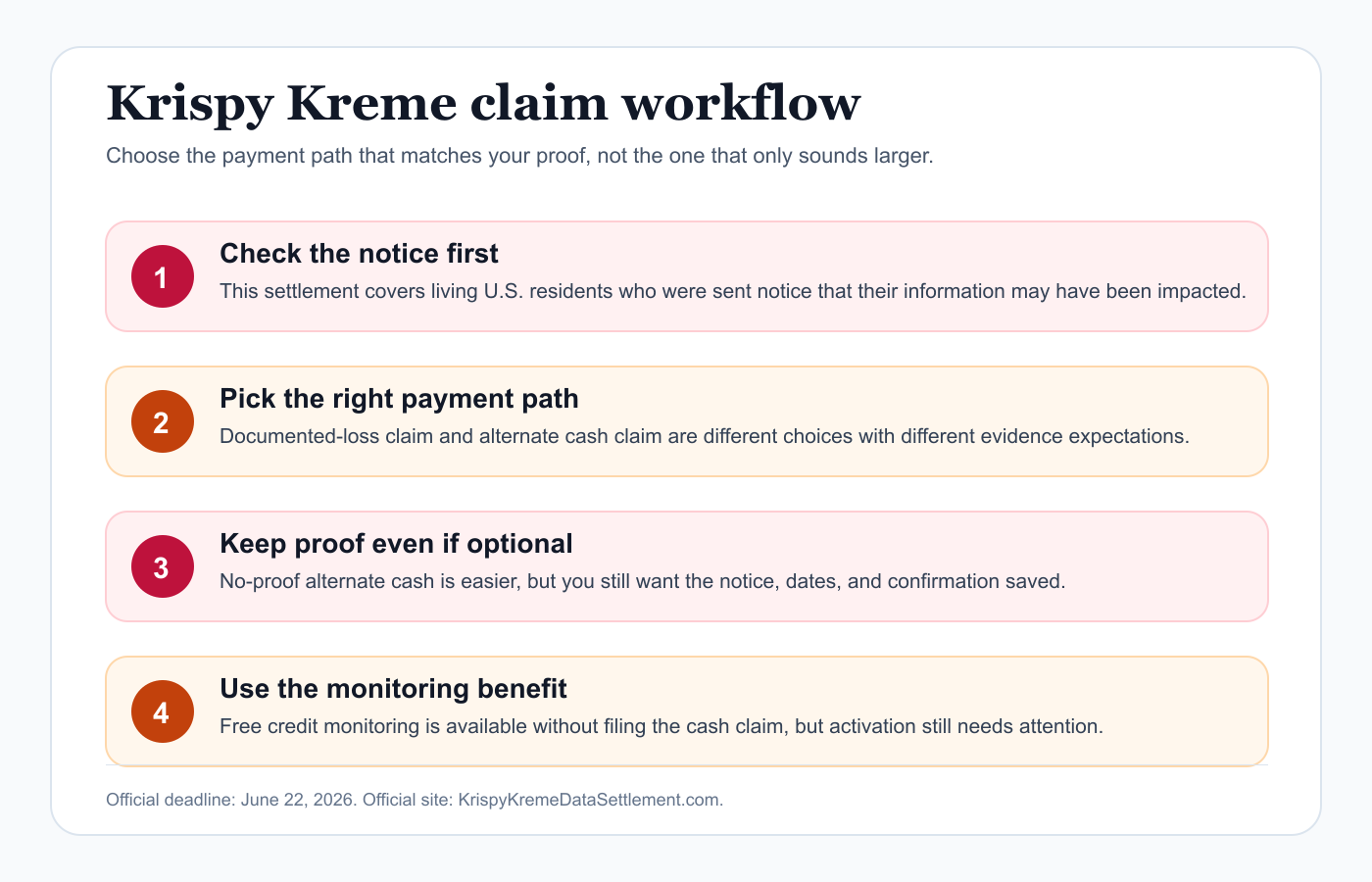

- Open the official settlement website or notice documents directly and confirm that your claim deadline is June 22, 2026.

- Check whether you were sent a notice of the Data Incident. The official postcard notice defines the covered class around notice recipients.

- Decide whether you are filing for documented losses, the alternate cash payment, or just activating monitoring. Do not start the form until you know which path you are taking.

- If you are filing for documented losses, gather statements, invoices, bank records, fraud correspondence, or identity-theft expenses that show an unreimbursed monetary loss tied to the breach.

- If you are choosing the alternate cash option, still save the notice and confirmation even though the path does not require the same level of documentation.

- Activate the free credit monitoring if you qualify and have the activation code, even if you also file a cash claim.

- Submit the claim before June 22, 2026 and save the final confirmation number, screenshots, and payment election details.

- If your claim is partially denied, keep your records so you can respond quickly to any administrator request for clarification.

The main discipline here is picking the right lane early. Many claim problems happen because consumers start with the bigger number in mind instead of the proof standard in front of them.

Comparison Table

| Benefit Path | Best For | What You Usually Need | Main Tradeoff |

|---|---|---|---|

| Cash Payment A | Consumers with documented fraud or identity-theft-related losses | Statements, invoices, receipts, fraud records | Higher upside, more scrutiny |

| Cash Payment B | Consumers who qualify but do not have loss documentation | Basic valid claim submission | Lower payout, simpler filing |

| Credit Monitoring | Consumers who want ongoing monitoring after notice | Activation code or notice details | No immediate cash by itself |

| Do Nothing | People who decide not to participate | Nothing | No payment and no monitoring activation |

Checklist and Security Callout

Before you file, decide whether you are making a proof-heavy claim or a proof-light claim.

- Official deadline June 22, 2026 is verified.

- Notice letter or notice email is saved.

- You have chosen documented losses or alternate cash before starting.

- Loss documentation is organized if using the higher-dollar path.

- Credit monitoring activation details are saved.

- Claim confirmation will be captured before you close the browser.

Tip: The bigger number is not always the better claim. If your losses are weakly documented, an aggressive documented-loss submission can stall or fail, while a clean alternate-cash claim may actually get paid faster.

Consumers often under-document time-sensitive fraud cleanup. If you had to replace a card, pay for postage, buy monitoring, spend money freezing credit, or absorb bank fees, gather those records now while they are easy to find. Waiting until the week of the deadline almost guarantees that some records will go missing.

If someone else in your household received the notice, make sure the claim is being filed under the correct person. Data breach notices often go to the name in the breached dataset, not necessarily the person who opens the mail today.

This is also a good example of why settlement claims and merchant refund requests are different. Krispy Kreme support is not the place to resolve a court-supervised settlement payout question. Use the administrator process for the settlement, and use normal merchant or bank channels only for unrelated, current billing problems.

The same file hygiene that helps with breach settlements also helps with charge disputes. Dates, amount fields, official notices, and clear loss records create leverage. Vague descriptions create delay.

Product Connection

LaimRefund is designed for disputes where the money path is unclear. If you are not sure whether to pursue a settlement claim, a merchant refund, or a bank dispute, the tool helps organize the facts so you can choose the right route first.

It is especially helpful when you need to write a structured appeal instead of a narrative rant. That can matter a lot in subscription, travel, and billing cases where the first denial is mostly a formatting problem disguised as a policy problem.

Scan your domain now. Ten seconds.

FAQ Section

What is the Krispy Kreme claim deadline?

The official postcard notice says online claims or mailed claims must be submitted or postmarked by June 22, 2026.

Do I need proof to get money from the Krispy Kreme settlement?

It depends on which option you choose. Documented-loss claims need reasonable supporting proof, while the alternate cash option is the lower-friction path described in the notice.

Who qualifies for the Krispy Kreme data breach settlement?

The official notice says it covers living individuals residing in the United States who were sent a notice indicating their private information may have been impacted in the Data Incident.

Should I file for the $3,500 maximum or the alternate cash option?

Choose the documented-loss path only if you have records tying unreimbursed losses to the breach. If not, the alternate cash option may be the cleaner claim.

Is the Krispy Kreme settlement website real?

Verify the case name, phone number, and deadline against the official notice. Use the official settlement site and avoid any site asking for fees or unrelated credentials.

Related Internal Links

- AT&T $177 Million Data Breach Settlement: How Customers Can Claim Money Without Losing Proof

- Fidelity $2.5 Million Data Breach Settlement: How Customers Can Claim Up to $5,000 Without Getting Denied

- Check Your Refund Case

Source: In re Krispy Kreme Data Breach Litigation Official Notice (June 2, 2026). Official postcard notice for the Krispy Kreme settlement benefits and June 22, 2026 deadline

More Refund Guides

Getting double charged for a single purchase is scary but fixable...

GoDaddy auto-renewed my domain at a high price. Learn how to get your money back....

This is my story of fighting Motel 6 for $1304. Learn how to get your money back....