By LaimRefund Team · June 05, 2026

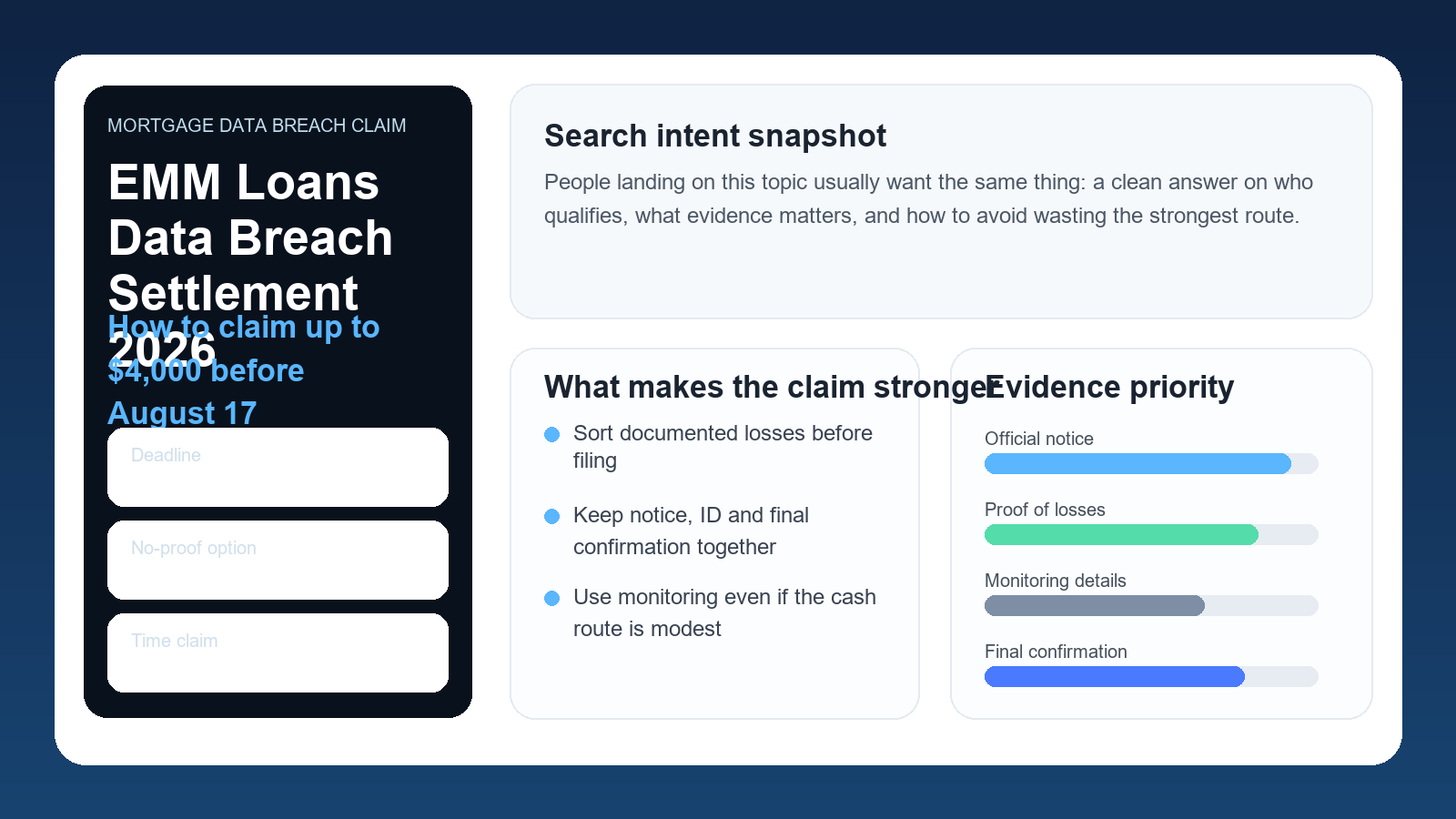

EMM Loans Data Breach Settlement 2026: How to Claim Up to $4,000 Before August 17

People searching for the EMM Loans data breach settlement in 2026 usually want a practical answer, not a legal lecture. They want to know whether the notice is real, whether the $4,000 headline number is realistic, what documents actually count, and whether it is smarter to choose the alternative cash payment instead of overreaching with a weak documented-loss claim.

Introduction and Main Problem Explanation

ClassAction.org reported on June 3, 2026 that EMM Loans agreed to a settlement covering people whose personally identifiable information was implicated in the lender's February 2024 data breach. That immediately creates the exact search behaviour this page is built for: EMM Loans settlement, EMM Loans data breach claim, EMM Loans claim form, and EMM Loans $4,000 settlement proof. Those are high-intent searches because the reader is already trying to decide whether to file or whether the filing is worth the work.

The first practical problem is that a settlement headline compresses several different benefits into one figure. In the EMM Loans case, the largest advertised recovery is tied to documented out-of-pocket losses, while an easier alternative cash payment is available without the same level of proof. Consumers often mix those together. They either rush at the bigger number with weak records, or they undersell their claim and take the easier route without checking whether their fraud-related costs could support more.

A mortgage-related breach also feels heavier than some retail breaches because the records involved can include Social Security numbers, state identification numbers and passport numbers. That changes how people think about loss. The reader is not only asking whether there is money on the table. They are also asking whether the administrative work of filing is worthwhile when the bigger concern may be long-tail identity misuse. A useful article needs to respect both concerns.

The strongest claim files usually begin with subtraction, not addition. Before a consumer starts attaching every scary-looking document, they should separate what is clearly tied to the breach from what merely happened after the breach. For example, a replacement ID fee, credit freeze charge, fraud-resolution cost or account-monitoring expense can make obvious sense. A vague sense that life was disrupted, without receipts or records, is harder to turn into compensable value.

This distinction matters because claim administrators are not evaluating emotion. They are matching people to a settlement class, reviewing deadlines, and deciding whether the submitted evidence satisfies the specific rules in the settlement materials. If your records look tidy to a stranger, your chances improve. If the file reads like a general complaint about stress and inconvenience, the biggest number on the page becomes much harder to reach.

Timing matters as well. Settlement deadlines feel distant until they suddenly do not. August 17, 2026 may sound comfortable now, but people regularly lose claims by waiting until the final week and then discovering that the notice letter, login ID, bank statements or supporting receipts are not where they thought they were. Search-led content should therefore encourage evidence preservation immediately rather than treating the claim as a task for later.

Searchers also need a plain-English explanation of the time claim. The EMM Loans settlement allows compensation for up to three hours of lost time at a set hourly rate, subject to the overall cap. That sounds simple until a consumer asks what kind of time counts. The safest answer is to document time tied to a concrete response to the breach: freezing credit, dealing with fraud alerts, replacing identification, speaking to financial institutions, or resolving misuse linked to the incident.

This is exactly where manual review tends to break down for ordinary people. They can see the notice, the website, the bank statement and the policy page, yet still struggle to decide which path is strongest. That is not because the claim is intellectually impossible. It is because the process is split across too many systems. The practical job of a good SEO page is to reduce that complexity into a sequence that a tired person can follow without making the claim worse.

The title has to reflect that real search intent. Readers are not searching for a clever headline. They are searching for the company name, the year, the benefit range, and the claim deadline because those are the terms that help them recognise the issue instantly.

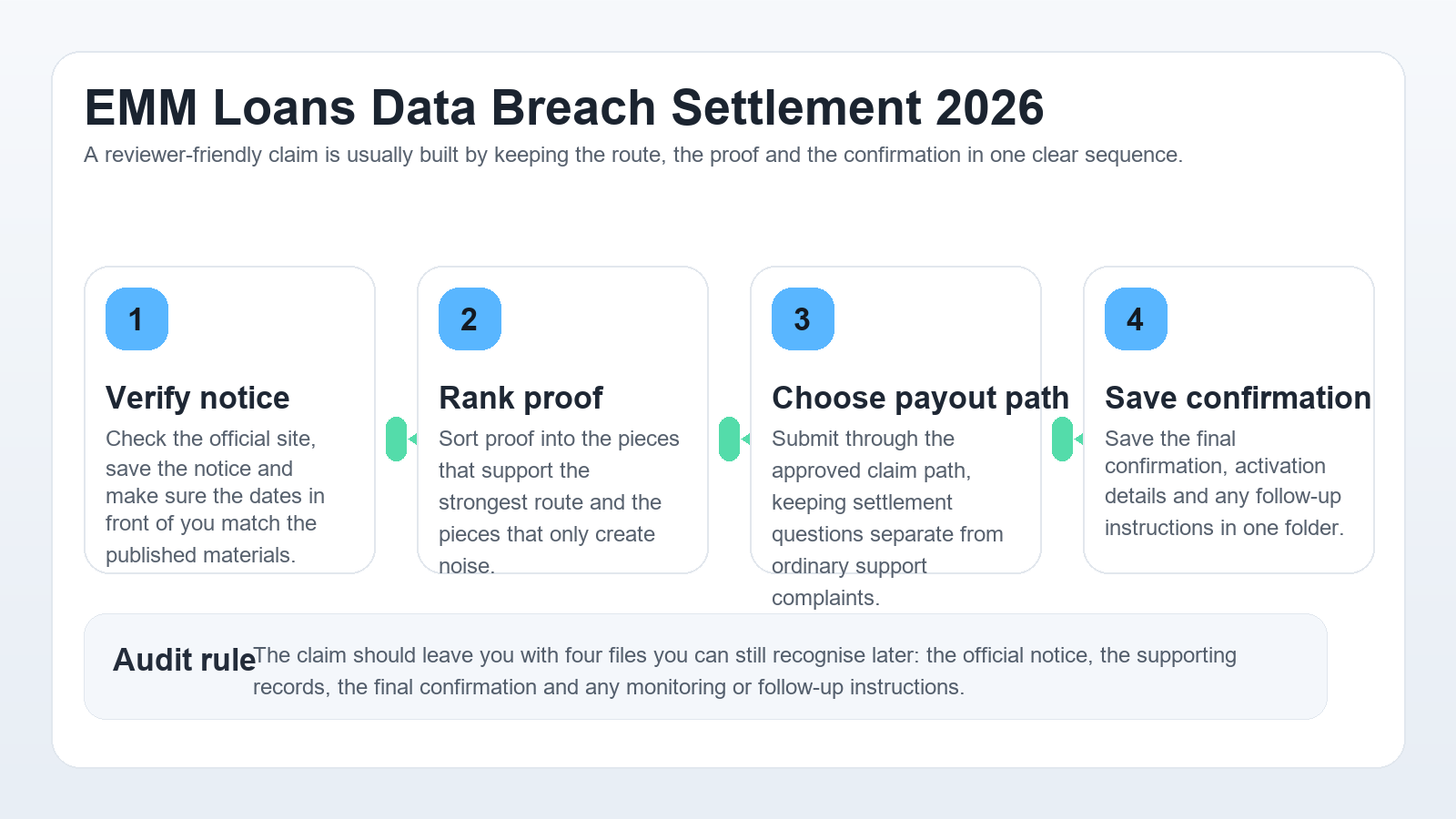

Step-by-Step Guide

- Go to the official EMM Loans settlement site and confirm the claim deadline is August 17, 2026 before doing anything else.

- Check whether you received notice that your information was implicated in the February 2024 breach, and save that notice in PDF or screenshot form.

- Sort your possible losses into three groups: documented out-of-pocket losses, documented response time, and weak or unprovable costs.

- If you have strong proof such as receipts, statements or invoices tied to breach response, prepare a documented-loss claim instead of defaulting to the alternative cash option.

- If your records are light but you still qualify, consider the $50 alternative cash payment rather than forcing a weak higher-value submission.

- Record any time spent on credit freezes, ID replacement, bank calls or fraud resolution if it clearly relates to the breach response.

- Submit the claim before August 17, 2026 and save every confirmation page, uploaded file and reference number.

- After filing, keep the confirmation and any monitoring details together so you can respond quickly if the administrator asks follow-up questions.

The point of the steps below is not to turn a settlement into a dramatic event. It is to keep the claim factual, narrow and easy to verify.

Comparison Table

| Claim Path | Best For | Typical Proof | Main Risk |

|---|---|---|---|

| Documented losses | Consumers with unreimbursed fraud or breach-response costs | Receipts, invoices, bank statements, ID replacement records | Weak causation between the cost and the breach |

| Lost time | Consumers who spent real time responding to the incident | A dated activity log plus supporting context | Claiming vague stress instead of documented response work |

| Alternative cash payment | Consumers who qualify but do not have strong records | Valid class claim submission | Leaving money on the table if stronger proof exists |

| Credit monitoring | Consumers who want practical protection beyond cash | Notice and activation details | Ignoring the benefit because it is not an immediate payout |

Checklist and Security Callout

Before you submit anything, build one file that proves the class link, the claimed losses and the final submission trail.

- The notice or eligibility email is saved.

- The August 17, 2026 deadline is written down.

- Losses are sorted by proof strength.

- Time spent responding to the breach is logged separately.

- The chosen payment path matches the available records.

- Final claim confirmation will be saved immediately after filing.

Tip: the most common EMM Loans mistake is chasing the $4,000 headline with weak records. A smaller, cleaner claim is often stronger than a larger claim built on assumptions.

The cleanest EMM Loans claim packet usually contains the notice, the official settlement URL, a screenshot of the key deadlines, the proof for whichever payment path you choose, and the final confirmation after submission. That sounds basic, but this exact file structure prevents most avoidable errors.

Scam risk is also real with breach settlements because the notices often arrive from unfamiliar administrators and direct users to standalone websites. A legitimate-looking message can still feel suspicious, especially when money and sensitive information are involved. The safest habit is to type the official site into the browser yourself or verify it against a trusted publication before entering anything.

Do not inflate losses in the hope that a larger number will sound more persuasive. Administrators respond better to a restrained claim that is fully documented than to a grand claim full of assumptions. A modest file with clean proof is much more likely to survive review than a dramatic one held together by guesswork.

The alternative cash option should also be treated seriously. Some people hear no proof required and assume it is the lesser path by definition. In reality, it can be the smarter path when your fraud response was limited, your receipts are thin, or your time records are weak. Matching the evidence to the path is almost always better than forcing the wrong path to fit.

This is why search-driven guidance should always end in action, not abstraction. The consumer does not need a reminder that breaches are bad. They need help deciding what to save, what to file, and what to avoid.

Product Connection

This is exactly the kind of case where LaimRefund can be useful even though the issue is a settlement rather than a standard merchant refund. The hard part is not recognising that something went wrong. The hard part is deciding which money path matches the evidence and then presenting that path cleanly.

Manual review often collapses when people mix class membership, fraud response, emotional stress and unrelated expenses into one bundle. LaimRefund helps turn that muddle into a clearer timeline and a narrower claim story, which is often the difference between a submission that looks reviewable and one that stalls.

Scan your domain now. Ten seconds.

FAQ Section

What is the EMM Loans claim deadline in 2026?

The EMM Loans settlement claim deadline is August 17, 2026 according to the official settlement materials highlighted by ClassAction.org.

Do I need proof to claim up to $4,000 from the EMM Loans settlement?

Yes. The higher documented-loss path requires proof such as receipts, statements or other records showing unreimbursed costs tied to the breach.

Can I choose the EMM Loans $50 cash option instead?

Yes. The settlement materials describe a $50 alternative cash payment for class members who prefer the simpler route instead of a documented-loss submission.

What kind of time can count in an EMM Loans claim?

The safest time claims are tied to concrete breach response work, such as freezing credit, replacing identification or speaking with financial institutions about misuse.

Is the EMM Loans settlement website real?

Verify the site name, deadline and notice details against the official notice or a trusted publication before entering personal information.

Related Internal Links

- Family Medicine Centers Data Breach Settlement 2026: How to Claim Cash and Monitoring

- Krispy Kreme Data Breach Settlement 2026: How to Claim Before June 22

- Check Your Refund Case

Source: ClassAction.org (June 3, 2026). EMM Loans Settlement Ends Class Action Lawsuit Over February 2024 Data Breach

More Refund Guides

I want to share how I got $509 back from Hoka...

When Netflix denied my $191 refund I read their entire policy and consumer laws...

Standard script: policy this, terms that. Learn how to get your money back....