By LaimRefund Team · June 02, 2026

SouthState Bank Data Breach Settlement 2026: How to Claim Before June 15

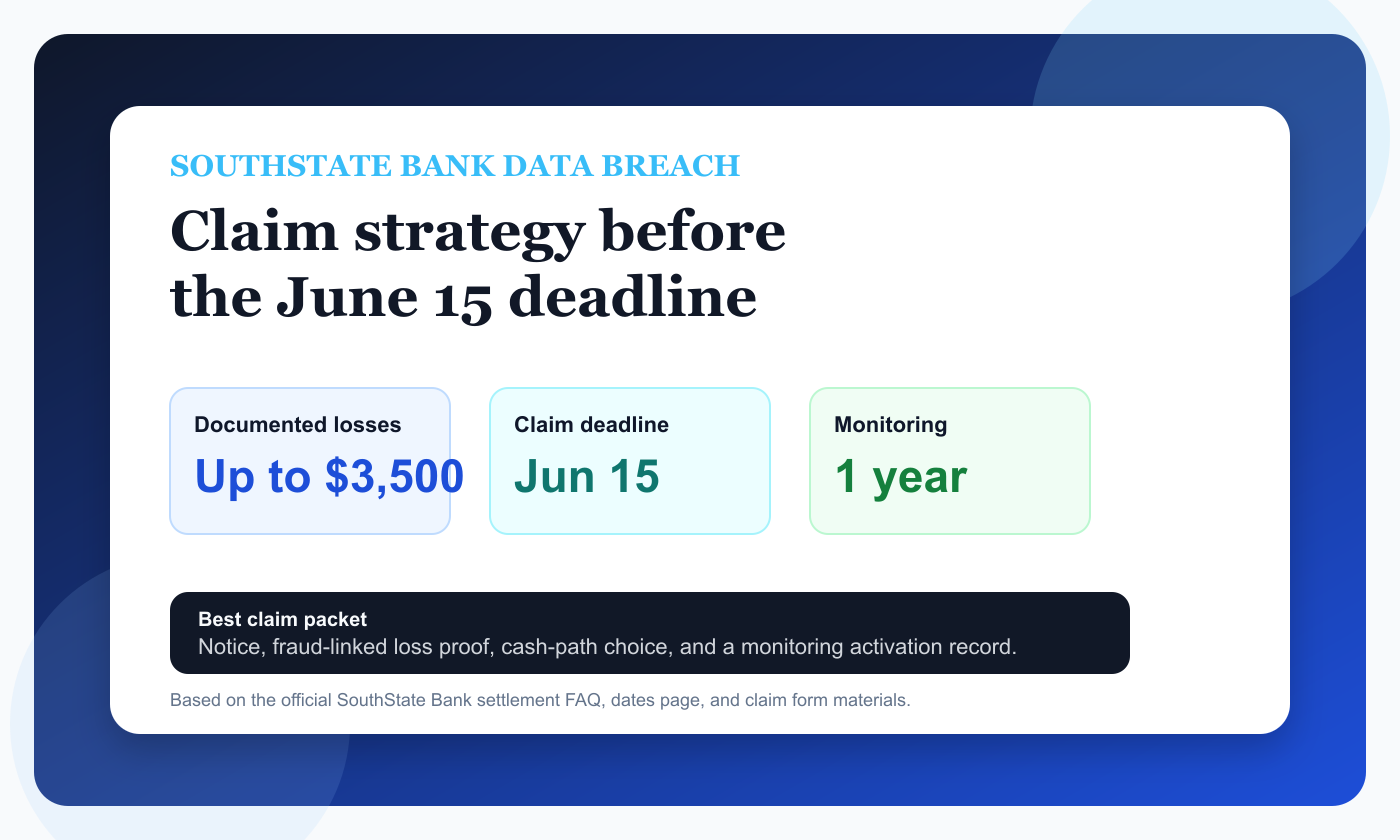

SouthState Bank's settlement closes on June 15, 2026, and the main consumer decision is whether to pursue documented losses up to $3,500, rely on the pro rata cash payment, or at least secure the one-year monitoring benefit. The best result usually comes from sorting losses by proof strength before you touch the form.

Introduction and Main Problem Explanation

The official SouthState Bank settlement materials say the claim deadline is June 15, 2026 and that class members may be eligible for up to $3,500 in documented out-of-pocket losses more likely than not caused by the Data Incident, plus a pro rata cash payment and one year of credit monitoring protection. The official FAQ also says claimants should provide reasonable third-party documentation such as credit card statements, bank statements, invoices, telephone records, and receipts.

That is exactly the kind of language that confuses otherwise careful consumers. The phrase 'up to $3,500' sounds simple, but it masks a proof question. The administrator is not paying a flat $3,500 because a breach happened. The administrator is reviewing whether a particular loss was real, documented, unreimbursed, and more likely than not caused by the incident.

This is why the highest-signal work is classification. Some losses belong in the documented-loss bucket. Some belong in the pro rata cash bucket because the proof chain is weak. And some benefits, such as monitoring, should be activated even if the cash claim is modest. Treating those options as interchangeable often leads to sloppy submissions and avoidable denials.

There is also a timing issue. Banking-related losses generate records quickly, but they also get scattered quickly across statements, alerts, screenshots, fraud reports, and card-reissue notices. If consumers wait until the last two days before the deadline, they often remember the incident but cannot reconstruct the record trail well enough to support the higher-dollar path.

The fastest way to lose money in a settlement is to confuse the claim path with the story path. The story path is what happened to you. The claim path is what the administrator actually needs to approve payment: a class definition match, a deadline, and the right identifiers.

Consumers also tend to over-assume that a no-proof claim means no records matter. In reality, records still protect you if the administrator asks follow-up questions, if your notice was lost, if your address changed, or if you later need to choose between a flat payment and a documented-loss claim.

A disciplined file usually includes five things: the notice email or letter, the official settlement URL typed directly into the browser, a screenshot of the important dates page, any receipts or statements tied to the issue, and a copy of the final claim confirmation. That packet is much more useful than relying on memory weeks later.

Scam risk is part of the workflow now. Real settlements often look odd because they use standalone domains, third-party administrators, and claim IDs. That means a legitimate notice can feel suspicious. The safe move is not to ignore every message. The safe move is to verify the case name, administrator, deadline, and official website before you type anything.

Search demand around these topics is practical and urgent. People search for whether a settlement is real, what deadline applies, whether proof is required, how much documented losses are worth, and whether they can still sue if they do nothing. A strong SEO article has to answer those concrete questions in plain language.

Searchers landing on this topic are usually not browsing. They want a tactical answer to a tactical question: is this settlement real, what proof counts, do I need receipts, and how do I decide between the easy claim and the stronger claim? That is why the article needs to stay concrete.

Step-by-Step Guide

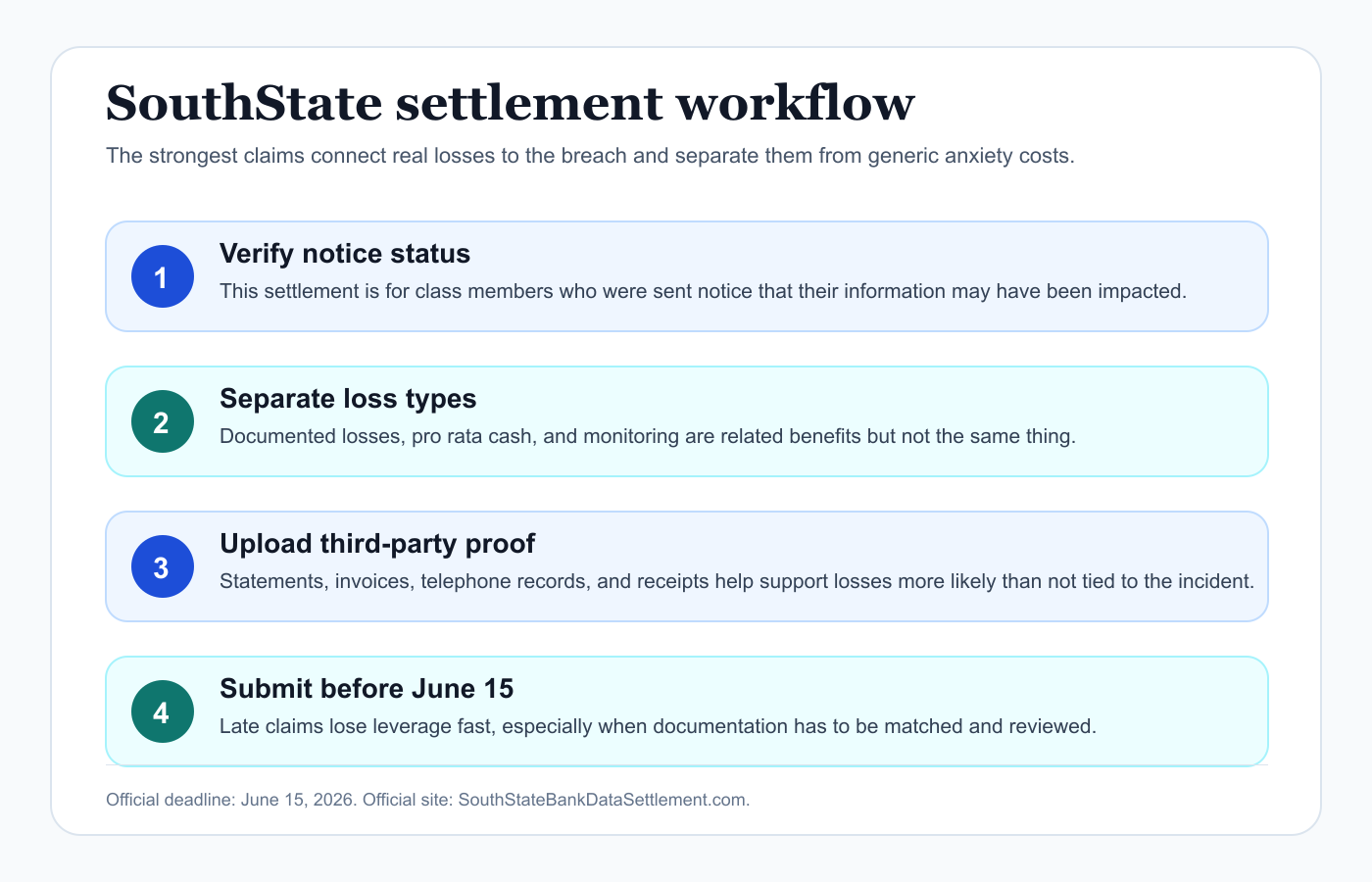

- Open the official SouthState Bank settlement site and confirm the claim deadline is June 15, 2026.

- Check that you were sent notice that your information may have been impacted. The settlement class is built around notice recipients.

- List every potential loss you think might connect to the breach, then sort those losses into documented, partially documented, or weakly documented categories.

- For documented losses, gather third-party proof such as bank statements, invoices, receipts, and related records that show the expense was unreimbursed and tied to fraud or identity theft.

- Decide whether you are claiming documented losses, the pro rata cash payment, or both if the settlement materials allow both paths under your facts.

- Save the credit monitoring activation details and use them instead of assuming monitoring will handle itself later.

- Submit the form before June 15, 2026 and keep screenshots of every page, uploaded record, and final confirmation.

- If the administrator asks you to cure or clarify part of the claim, respond with the narrow missing proof instead of rewriting the whole story.

A settlement like this rewards evidence discipline. People who treat the claim like a short legal filing usually do better than people who treat it like a complaint form.

Comparison Table

| Benefit | Best Use Case | Typical Proof | Main Risk |

|---|---|---|---|

| Documented losses | You have unreimbursed fraud or identity-theft-related expenses | Statements, invoices, telephone records, receipts | Weak causation or missing third-party proof |

| Pro rata cash payment | You qualify but do not have strong loss documentation | Valid claim submission and class match | Lower payout than a strong documented claim |

| Credit monitoring | You want protective value even without cash proof | Activation information from the notice | Forgetting to activate before details get lost |

| Do nothing | You choose not to participate | None | No recovery and no monitoring benefit |

Checklist and Security Callout

Before you file, decide what can actually be proven rather than what merely feels related to the breach.

- June 15, 2026 deadline is verified.

- Notice letter or email is saved.

- Losses are sorted by documentation strength.

- Third-party records are gathered for the documented-loss path.

- Monitoring activation details are preserved.

- Final claim confirmation will be saved.

Tip: Do not inflate breach losses with vague time estimates or unrelated expenses. Administrators are much more receptive to smaller claims with tight proof than to oversized claims with a weak causation story.

A practical way to think about causation is this: if you had to show the loss to a bank investigator, would the documents make sense without a long speech? If yes, the record may be strong enough for the documented-loss path. If no, the pro rata route may be the cleaner play.

Bank-fee claims are often stronger than consumers expect because they can be shown directly on statements. The weak point is not always the fee itself. It is the bridge between the fee and the breach. Pair the fee with fraud alerts, card replacement records, or customer-service correspondence if you have them.

Credit monitoring also matters for people who have not yet seen direct losses. Settlements often pay small cash amounts but give benefits that are more practically useful if activated right away. Ignoring monitoring because it is not immediate cash can be a bad trade.

This is another good reminder that settlement claims and merchant refund requests serve different goals. The settlement is compensating a class under court supervision. It is not a normal customer-service refund. Use the official administrator path for the settlement, and keep your separate banking disputes in their own folder.

Product Connection

LaimRefund helps when a consumer needs to decide which money path actually fits the evidence. That can mean a settlement claim, a bank dispute, or a merchant refund request, and those are not interchangeable.

It is especially useful for turning scattered records into a sequence that a reviewer can follow. Good structure does not guarantee recovery, but bad structure quietly kills a lot of claims.

Scan your domain now. Ten seconds.

FAQ Section

What is the SouthState Bank claim deadline?

The official dates page lists June 15, 2026 as the claim deadline.

What counts as proof for SouthState documented losses?

The official FAQ points to reasonable third-party documentation such as bank statements, credit card statements, invoices, telephone records, and receipts.

Can I still file if I do not have documented losses?

Yes, the settlement materials also describe a pro rata cash payment path for class members, in addition to monitoring benefits, but you should verify the exact options on the official site.

Do I need to activate the monitoring separately?

Treat monitoring like a real benefit that needs attention. Save the activation details and complete that step instead of assuming it will happen automatically.

How do I know if the SouthState settlement site is real?

Verify the case name, deadline, contact information, and claim form flow against the official SouthState Bank settlement website before entering personal information.

Related Internal Links

- Comcast Xfinity $117.5 Million Data Breach Settlement: How to File a Strong Claim Before the Deadline

- Fidelity $2.5 Million Data Breach Settlement: How Customers Can Claim Up to $5,000 Without Getting Denied

- Check Your Refund Case

Source: SouthState Bank Data Settlement FAQ and Dates (June 2, 2026). Official SouthState Bank settlement claim deadline and documented-loss guidance

More Refund Guides

After writing dozens of refund emails to British Airways I have found a formula that works almost ev...

Planet Fitness requires you to cancel in person or by certified mail. Learn how to get your money ba...

I have written probably 50+ refund emails to Samsung over the years for myself and friends. Learn ho...